Business

PSX weekly review: Bulls dominate as KSE-100 index shoots past 42,000 mark

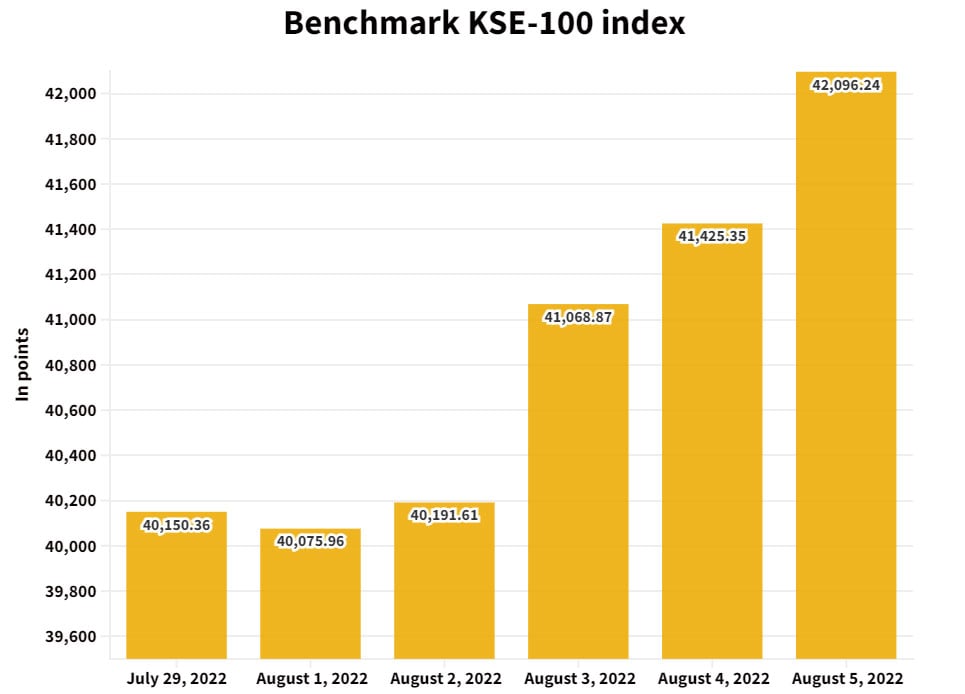

- KSE-100 index gains 1,946 points.

- Finishes four out of five sessions in green.

- Interest in main board sectors kept market buoyant.

KARACHI: The Pakistan Stock Exchange (PSX) recouped losses from the previous week with the benchmark KSE-100 index gaining 1,946 points or 4.9% to settle at 42,096.24. Trading remained volatile throughout the week with the index finishing four out of five sessions in the green.

Interest in main board sectors kept the market buoyant as investor participation remained strong. The index maintained a healthy momentum on back of trade deficit and strengthening rupee against the US dollar. Additionally, sector-specific developments also spurred buying interest in select stocks, which further fuelled the rally.

The market commenced the week on a negative note as inflation for the month of July 2022 came in at 24.9%, — highest level in last 14 years.

Fortunately, tables turned and the sentiment turned positive after the International Monetary Fund (IMF) announced that Pakistan had fulfilled the last remaining pre-requisite for the loan (incremental hike in petroleum development levy on MS and hi-speed diesel).

With this renewed hope, the Pakistani rupee strengthened against greenback, gaining Rs15.33, or 6%, week-on-week to close at Rs224.04 this week.

Furthermore, trade deficit significantly declined in July, down by 47% month-on-month. Moreover, reduction in international oil prices post OPEC+ meeting (WTI trading below $88 per barrel compared to $98.62 per barrel last week) further cemented the ground for bulls.

Other major developments during the week were: ministry agreed to increase oil marketing companies margin on MS (petrol), hi-speed diesel, SBP’s forex reserves fell $190 million to $8.4 billion, banks give Rs298 billion financing in PIB auction, refineries’ gross margin declined 83% in August, and oil sales in July 2022 clocked in at the lowest level since February 2021.

Meanwhile, foreign selling this week clocked in at $0.69 million against a net buy of $0.57 million recorded last week. Selling was witnessed in banks ($0.9 million), and fertiliser ($0.6 million).

On the domestic front, major buying was reported by brokers proprietary ($2.2 million), followed by mutual funds ($1.6 million).

During the week under review, average volumes clocked in at 263 million shares (up by 75% week-on-week), while average value traded settled at $34 million (up by 56% week-on-week).

Major gainers and losers of the week

Sector-wise positive contributions came from banks (+427 points), cement (+421 points), fertiliser (+112 points), chemical (+111 points), and oil marketing companies (+106 points).

On the flip side, negative contributions came from close-end mutual fund (-3 points), and real estate investment trust (-1 points).

Scrip-wise major gainers were Luck Cement (+155 points), UBL (+124 points), MCB (+87 points), PSO (+78 points), and Colgate-Palmolive (+73 points).

Meanwhile, major losers were Faysal Bank (-10 points), Mari Petroleum (-6 points), Interloop (-4 points), and Adamjee Insurance Company (-3 points).

Outlook for next week

A report from AHL predicted: “We expect the market to remain in the green zone given hopes on loan disbursement from IMF once approval is granted by the Executive Board.”

“Moreover, with the ongoing result season, certain sectors and scrips are expected to stay under the limelight given anticipation of robust results,” it said, advising investors to cherry-pick fundamentally strong blue-chip stocks.

“The KSE-100 is currently trading at a PER of 4.3x (2022) compared to the Asia-Pacific regional average of 12.5x while offering a dividend yield of 8.9% versus 2.8% offered by the region,” the brokerage house stated.

Minutes after taking off from Lahore airport, a private airline plane was “hit by a bird.”

Deputy Prime Minister to Represent Pakistan at CHOGM in Samoa in 2024

China Contributes 43 New Foreign Firms to the 6% Growth in SECP Registrations

Barwaan Khiladi: Kinza Hashmi discusses her role as Alia

Bannu Cantonment Board CEO Bilal Pasha ‘commits suicide’

Snap launches tools for parents to monitor teens’ contacts

Learn First | How to Create Amazon Seller Account in Pakistan – Step by Step

Sajjad Jani Funny Mushaira | Funny Poetry On Cars🚗 | Funny Videos | Sajjad Jani Official Team

Pakistan Reaction On Huge Win Against India | Pakistani Celebs Celebrate World T20 Cricket

-

Entertainment2 days ago

Entertainment2 days agoReham Khan’s counsel to Hania Amir between marriage versus career

-

Latest News2 days ago

Latest News2 days agoThe government and the military are successfully combating drug abuse through a nationwide anti-drug operation.

-

Latest News2 days ago

Latest News2 days agoAt a ceremony held at Mirpur, the Prime Minister of Jammu and Kashmir stated, “We will not hesitate to make any sacrifice for peace in the region.”

-

Latest News2 days ago

Latest News2 days agoThe 26th Amendment to the Constitution: The Amendment That Completes the Charter of Democracy: Bilawal

-

Latest News2 days ago

Latest News2 days agoIn the border region, a Lahore police officer was detained for allegedly using drones to smuggle drugs.

-

Entertainment2 days ago

Entertainment2 days agoThe Punjab government initiates the ‘Dhee Rani’ initiative for underprivileged couples.

-

Latest News2 days ago

Latest News2 days agoJudicial Appointments in the Supreme Court Will Be Made Transparent: Law Minister

-

Business23 hours ago

Business23 hours agoChina Contributes 43 New Foreign Firms to the 6% Growth in SECP Registrations