Business

Gold loses shine, price plunges by Rs4,200 per tola

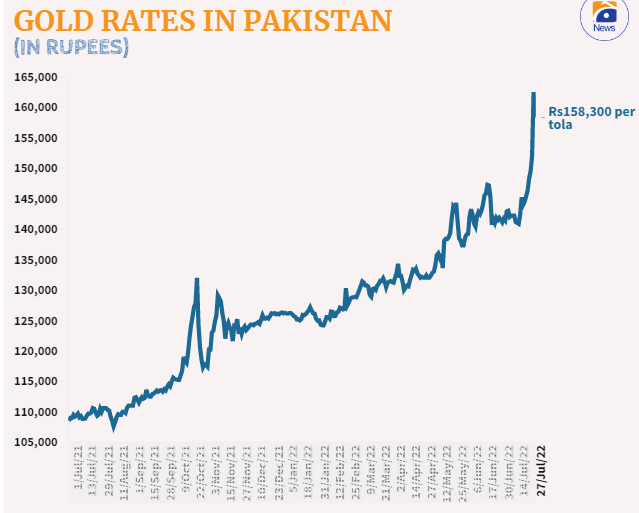

- Gold price settles at Rs158,300 per tola.

- Since Monday, gold gained Rs12,000 per tola.

- Silver prices in domestic market remain unchanged.

KARACHI: Gold lost its shine on Friday as the precious commodity receded nearly half of its gain recorded a day earlier as the Pakistani currency snapped its 10-day losing streak.

Data released by the All Sindh Saraf and Jewellers Association (ASSJA) showed that the price of gold, considered a safe haven, plunged by Rs4,200 per tola and Rs3,601 per 10 grams to settle at a record high of Rs158,300 and Rs135,717 in the local market.

A day earlier, the gold price jumped by a whopping Rs10,500 per tola and the price hit a historic-high of Rs162,500.

Cumulatively, since the start of the week — Monday — gold has gained Rs12,000 per tola in the local bullion market.

“Gold price is climbing high in the local bullion market in line with the prices in the international market — which has surged by $50 per ounce since Monday — and depreciation of Pakistani rupee against the US dollar,” AA Commodities Director Adnan Agar told Geo.tv a day earlier.

The analyst further said that the precious commodity is expected to maintain an uptrend as international prices are once again eyeing a $1,800 mark while there is “no hope of stability in local currency” till the country receives a loan tranche from the International Monetary Fund (IMF).

The association, however, stated that although gold hit an all-time high in Pakistan, its price still stood below cost. Gold is cheaper by Rs6,500 per tola compared to its price in Dubai.

The latest price for local markets was determined to keep in view the prices at which trades took place among buyers and sellers.

ASSJA President Haji Haroon Chand lamented that their businesses are suffering because of a lack of purchasing power; while the government has also imposed fixed taxes on gold dealers which is also adding to the woes of the dealers.

In the international market, bullion prices increased by $12 per ounce to settle at $1,762 supported by a softer dollar and bets that the Federal Reserve may cool the pace of rate hikes as economic risks deepen.

Meanwhile, silver prices in the domestic market remained unchanged at Rs1,630 per tola and Rs1,397.46 per 10 grams today.

Business

Trade Agreements Worth $10.70 Million Were Signed At Expo For Pakistan And Indonesia To Increase Their Trade With The Support Of SIFC

In the border region, a Lahore police officer was detained for allegedly using drones to smuggle drugs.

At a ceremony held at Mirpur, the Prime Minister of Jammu and Kashmir stated, “We will not hesitate to make any sacrifice for peace in the region.”

The 26th Amendment to the Constitution: The Amendment That Completes the Charter of Democracy: Bilawal

Barwaan Khiladi: Kinza Hashmi discusses her role as Alia

Bannu Cantonment Board CEO Bilal Pasha ‘commits suicide’

Snap launches tools for parents to monitor teens’ contacts

Learn First | How to Create Amazon Seller Account in Pakistan – Step by Step

Sajjad Jani Funny Mushaira | Funny Poetry On Cars🚗 | Funny Videos | Sajjad Jani Official Team

Pakistan Reaction On Huge Win Against India | Pakistani Celebs Celebrate World T20 Cricket

-

Entertainment21 hours ago

Entertainment21 hours agoReham Khan’s counsel to Hania Amir between marriage versus career

-

Latest News20 hours ago

Latest News20 hours agoThe government and the military are successfully combating drug abuse through a nationwide anti-drug operation.

-

Latest News20 hours ago

Latest News20 hours agoAt a ceremony held at Mirpur, the Prime Minister of Jammu and Kashmir stated, “We will not hesitate to make any sacrifice for peace in the region.”

-

Latest News20 hours ago

Latest News20 hours agoThe 26th Amendment to the Constitution: The Amendment That Completes the Charter of Democracy: Bilawal

-

Latest News20 hours ago

Latest News20 hours agoIn the border region, a Lahore police officer was detained for allegedly using drones to smuggle drugs.

-

Latest News20 hours ago

Latest News20 hours agoJudicial Appointments in the Supreme Court Will Be Made Transparent: Law Minister

-

Latest News20 hours ago

Latest News20 hours agoPakistan’s Deputy Prime Minister will be present at the Commonwealth Heads of Government Meeting, which will take place in Samoa.

-

Entertainment21 hours ago

Entertainment21 hours agoThe Punjab government initiates the ‘Dhee Rani’ initiative for underprivileged couples.