Business

Rupee shatters all previous records, falls to new low of 221.99 against dollar

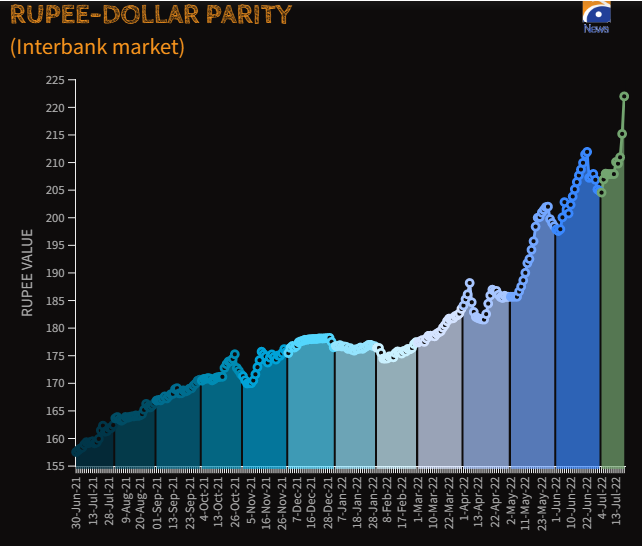

- Pakistani rupee falls by Rs6.79, closes at 221.99 against dollar.

- This is the highest day-on-day depreciation after June 26, 2019.

- Import pressure, political uncertainty behind rupee’s downfall.

The Pakistani rupee shattered all previous records on Tuesday, falling to a new low of 224 against the dollar in afternoon interbank trade, before closing at 221.99.

According to State Bank of Pakistan, the local currency fell by Rs6.79 in the interbank market, depreciating by 3.06% against yesterday’s close of Rs215.20.

It was the highest day-on-day depreciation after June 26, 2019 when the currency fell by Rs6.80.

The ruling PML-N’s thumping in the Punjab by-elections has triggered political uncertainty along with import pressure taking the Pakistani rupee on a downward trajectory.

Analysts believe, however, that the domestic political and economic situation are not the only factors at play.

“The dollar is getting stronger in the global market almost against all the world currencies and the Pakistani rupee is not the exception,” said Alpha Beta Core CEO Khurram Schezad.

Speaking of Pakistan’s financial situation, Schezad said that the country’s external account issues “are not settled as yet, the IMF (International Monetary Fund) is yet to be on board, and the flows are yet to materialise”.

“Global rating agencies have put a negative outlook on the economy, so that is an additional burden that is weighing on the financial markets in general and foreign exchange market in particular,” he added.

Exchange Companies Association of Pakistan (ECAP) Chairperson Malik Bostan Malik Bostan told Geo.tv that there were three reasons behind the constant devaluation of the local unit.

The forex expert said that investors are jittery at the moment as the Opposition PTI has bagged more seats than the PML-N in the Punjab by-polls — creating uncertainty over the future of the current set-up.

Bostan said that the speculations that the IMF’s Executive Board approval would take time and the money lender’s statement of being ready to negotiate with a caretaker government have exacerbated the devaluation.

He also pointed out that since the Taliban took over Afghanistan, Pakistan has provided them trade relief, resulting in additional pressure on the rupee.

The currency trader said that the State Bank of Pakistan (SBP) cannot intervene in the rising rupee-dollar parity as the country has agreed that the central bank will not intervene in the matter.

“…but even if it wishes to intervene, the SBP does not have enough dollars to inject into the market,” he said, adding that if the government wants to save the rupee, it will have to curtail the imports.

Minutes after taking off from Lahore airport, a private airline plane was “hit by a bird.”

Deputy Prime Minister to Represent Pakistan at CHOGM in Samoa in 2024

China Contributes 43 New Foreign Firms to the 6% Growth in SECP Registrations

Barwaan Khiladi: Kinza Hashmi discusses her role as Alia

Bannu Cantonment Board CEO Bilal Pasha ‘commits suicide’

Snap launches tools for parents to monitor teens’ contacts

Learn First | How to Create Amazon Seller Account in Pakistan – Step by Step

Sajjad Jani Funny Mushaira | Funny Poetry On Cars🚗 | Funny Videos | Sajjad Jani Official Team

Pakistan Reaction On Huge Win Against India | Pakistani Celebs Celebrate World T20 Cricket

-

Entertainment2 days ago

Entertainment2 days agoReham Khan’s counsel to Hania Amir between marriage versus career

-

Latest News2 days ago

Latest News2 days agoThe government and the military are successfully combating drug abuse through a nationwide anti-drug operation.

-

Latest News2 days ago

Latest News2 days agoAt a ceremony held at Mirpur, the Prime Minister of Jammu and Kashmir stated, “We will not hesitate to make any sacrifice for peace in the region.”

-

Latest News2 days ago

Latest News2 days agoThe 26th Amendment to the Constitution: The Amendment That Completes the Charter of Democracy: Bilawal

-

Latest News2 days ago

Latest News2 days agoIn the border region, a Lahore police officer was detained for allegedly using drones to smuggle drugs.

-

Entertainment2 days ago

Entertainment2 days agoThe Punjab government initiates the ‘Dhee Rani’ initiative for underprivileged couples.

-

Latest News2 days ago

Latest News2 days agoJudicial Appointments in the Supreme Court Will Be Made Transparent: Law Minister

-

Business23 hours ago

Business23 hours agoChina Contributes 43 New Foreign Firms to the 6% Growth in SECP Registrations