Business

Pakistan’s default odds rise as IMF sours on bailout: Bloomberg

- Report says without IMF programme, options for fresh funding will likely be “very limited.”

- “With forex reserves likely below $4bn, default seems highly likely,” reports mentions.

- Negotiations with IMF on any new bailout aren’t likely to start until after elections in October.

KARACHI: The International Monetary Fund’s (IMF) criticism of Pakistan’s latest budget suggests chances are rising that the lender will opt not to deliver long-awaited aid before its bailout programme finishes at the end of June, Bloomberg reported.

“This would cause a severe dollar shortage in the first half of the fiscal year that starts in July, and possibly for longer — significantly raising the odds of default, Bloomberg economist Ankur Shukla said in the report, Pakistan Insight.

“It would also raise the prospect of much lower growth, and higher inflation and interest rates than we currently anticipate in fiscal 2024.”

The IMF criticised the budget for not taking enough steps to broaden the tax base and for including a tax amnesty.

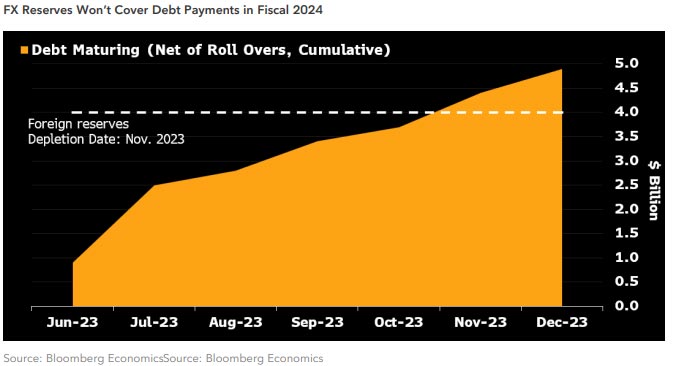

The country’s foreign currency reserves currently stand at $4 billion. With at least around $900 million in debt that must be repaid this month, the reserves will fall by June-end unless the IMF aid comes.

Between July-December, Pakistan must repay an additional $4 billion, which cannot be rolled over. “With foreign exchange reserves likely below $4 billion at the start of fiscal 2024, the default seems highly likely,” the report said.

“Without any IMF programme, the options for fresh external funding will likely be very limited.”

It said that negotiations with the IMF on any new bailout aren’t likely to start until after elections in October. “Reaching an agreement will take time. Any actual aid disbursement from the IMF under a new programme will not happen until December.”

In the meantime, the country will need to conserve dollars by limiting import purchases — and keeping a current account balance in surplus— to have any hope of being able to meet its obligations.

It will also need to seek assistance from friendly nations to avert a default in the first half of fiscal 2024.

The report said Pakistan’s economy will likely be hit hard if the IMF doesn’t deliver aid by June-end.

The authorities will have to keep import restrictions in place. The State Bank of Pakistan will also likely raise rates above the current level of 21% to further curb demand for imports and conserve foreign exchange reserves, it added.

“Our base case currently is that the SBP will likely remain on hold through December (but that assumed the IMF aid coming in by June-end).”

Continued import restrictions and a weaker rupee would lead to higher inflation in fiscal 2024 than currently anticipated.

“We currently expect inflation to average 22%. Higher borrowing costs and restrictions on imports of raw materials would hit production further. Higher inflation would damp consumption,” it added.

The report said if IMF aid doesn’t come this month, the growth will be much weaker in fiscal 2024 than the current forecast of 2.5%.

“Higher rates will also increase the government’s debt servicing costs. The government currently plans to spend half of the fiscal 2024 budget on debt servicing.”

Business

An investigation was “launched” into PTA’s inability to get Rs. 78 billion back from Telcos

Rainfall throughout the night stops flights in Lahore.

Containers were used to seal the Red Zone before JI’s sit-in at D-Chowk.

Changes to Pakistan’s Test team could be significant for the Bangladesh series.

Barwaan Khiladi: Kinza Hashmi discusses her role as Alia

Snap launches tools for parents to monitor teens’ contacts

Bannu Cantonment Board CEO Bilal Pasha ‘commits suicide’

Learn First | How to Create Amazon Seller Account in Pakistan – Step by Step

Sajjad Jani Funny Mushaira | Funny Poetry On Cars🚗 | Funny Videos | Sajjad Jani Official Team

Pakistan Reaction On Huge Win Against India | Pakistani Celebs Celebrate World T20 Cricket

-

Latest News3 days ago

Latest News3 days ago52 districts in Pakistan have 52 cases of the polio virus.

-

Latest News3 days ago

Latest News3 days agoFederal Cabinet once again postpones decision on PTI suspension and Article 6 action against Imran and Alvi

-

Entertainment3 days ago

Entertainment3 days agoA glimpse of Sania Mirza’s relaxed moments

-

Latest News3 days ago

Latest News3 days agoElection Amendment Act Case Heard by IHC; Response Requested From Law Ministry, ECP Within Ten Days

-

Latest News3 days ago

Latest News3 days agoThe 10th Executive Committee Meeting of SIFC examines the role of provinces in bringing in foreign investment.

-

Latest News3 days ago

Latest News3 days agoCabinet will probably decide today whether to ban PTI: Fawad ChaudhryCabinet will probably decide today whether to ban PTI: Fawad Chaudhry

-

Latest News3 days ago

Latest News3 days agoMubarak Sani Case: Punjab Government’s Review Petition Accepted by the SC

-

Latest News3 days ago

Latest News3 days agoPakistan has advanced to the Women’s Asia Cup 2024 semifinals.