Business

Bulls stage comeback at PSX on Ishaq Dar’s cues

- Investors cheer Dar’s assurance Pakistan will not seek debt restructuring from Paris club.

- Benchmark KSE-100 index traded between hope and despair.

- Investors kept a close watch on SBP’s decision on monetary policy.

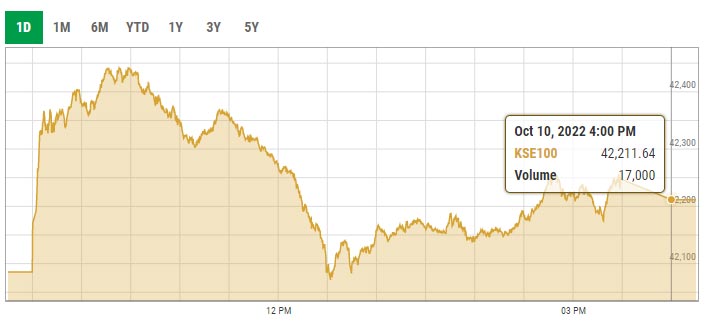

KARACHI: The bulls staged a comeback at the Pakistan Stock Exchange (PSX) on Monday cheering Finance Minister Ishaq Dar’s assurance that Pakistan will not seek debt restructuring from the Paris club.

Constant assurance from the top leadership that Pakistan will not seek debt restructuring from Paris Club creditor nations enticed market participants.

Moreover, Dar dismissed market rumours that the government might extend maturities for its bonds, saying that the country will fulfil all multilateral, international and bond obligations.

The benchmark KSE-100 index traded between hope and despair, which eventually let loose the bulls, who pulled the bourse into the green.

Investors kept a close watch on the State Bank of Pakistan’s decision on the monetary policy — which was later kept unchanged at 15% for the next seven weeks.

The KSE-100 index gained since the morning bell rang, but some dips were seen at regular intervals. The downtrend turned steeper at midday bulls managed to regain control.

The benchmark KSE-100 index closed at 42,211.64 points with an increase of 126.39 points or 0.30%.

Topline Securities in its post-market commentary noted that the KSE-100 index largely traded in the positive zone due to Dar’s statement regarding Pakistan not planning to seek a debt restructuring.

Shares of 336 companies were traded during the session. At the close of trading, 161 scrips closed in the green, 149 in the red, and 26 remained unchanged.

Overall trading volumes declined to 240.19 million shares compared with Friday’s tally of 313.34 million. The value of shares traded during the day was Rs10.53 billion.

Worldcall Telecom was the volume leader with 31.15 million shares traded, gaining Rs0.03 to close at Rs1.63. It was followed by Pak Elektron with 27.14 million shares traded, gaining Rs1.21 to close at Rs17.45 and TRG Pakistan with 26.74 million shares gaining Rs7.29 to close at Rs151.43.

Business

An investigation was “launched” into PTA’s inability to get Rs. 78 billion back from Telcos

Rainfall throughout the night stops flights in Lahore.

Containers were used to seal the Red Zone before JI’s sit-in at D-Chowk.

Changes to Pakistan’s Test team could be significant for the Bangladesh series.

Barwaan Khiladi: Kinza Hashmi discusses her role as Alia

Snap launches tools for parents to monitor teens’ contacts

Bannu Cantonment Board CEO Bilal Pasha ‘commits suicide’

Learn First | How to Create Amazon Seller Account in Pakistan – Step by Step

Sajjad Jani Funny Mushaira | Funny Poetry On Cars🚗 | Funny Videos | Sajjad Jani Official Team

Pakistan Reaction On Huge Win Against India | Pakistani Celebs Celebrate World T20 Cricket

-

Latest News3 days ago

Latest News3 days ago52 districts in Pakistan have 52 cases of the polio virus.

-

Latest News3 days ago

Latest News3 days agoFederal Cabinet once again postpones decision on PTI suspension and Article 6 action against Imran and Alvi

-

Entertainment3 days ago

Entertainment3 days agoA glimpse of Sania Mirza’s relaxed moments

-

Latest News3 days ago

Latest News3 days agoElection Amendment Act Case Heard by IHC; Response Requested From Law Ministry, ECP Within Ten Days

-

Latest News3 days ago

Latest News3 days agoThe 10th Executive Committee Meeting of SIFC examines the role of provinces in bringing in foreign investment.

-

Latest News3 days ago

Latest News3 days agoCabinet will probably decide today whether to ban PTI: Fawad ChaudhryCabinet will probably decide today whether to ban PTI: Fawad Chaudhry

-

Latest News3 days ago

Latest News3 days agoMubarak Sani Case: Punjab Government’s Review Petition Accepted by the SC

-

Latest News3 days ago

Latest News3 days agoPakistan has advanced to the Women’s Asia Cup 2024 semifinals.